From 2022 until December 2025, the Federal Reserve reduced its securities holdings by over $2 trillion, guided by the plans announced by the Federal Open Market Committee (FOMC) in May 2022. The FOMC ended this runoff when it decided reserves had reached an ample range. To maintain adequate reserve levels, the FOMC directed the Open Market Trading Desk at the New York Fed (the Desk) to increase System Open Market Account (SOMA) securities holdings through ongoing reserve management purchases (RMPs).

This article summarizes three sections from the 2025 SOMA Annual Report—released today—that explain how the Fed managed the transition to ample reserves, why it began RMPs, and how the public can track future balance sheet changes.

Shifting Market Indicators During 2025: The EFFR-IORB Spread

The amount of reserves that can be considered ample is a range and can vary over time. So, how does the Federal Reserve know when reserves are ample? To monitor reserve conditions, the Desk tracks various market prices and quantities and engages in discussions with market participants. One key indicator the Desk monitors is the spread between the effective federal funds rate (EFFR) and the interest rate paid on reserve balances (IORB). As the EFFR rises relative to IORB, it indicates that banks are willing to pay more to borrow reserves, signaling rising demand for reserves, declining supply of reserves, or both. As Box 1 in the SOMA Annual Report explains, this spread tightened considerably during the final months of 2025, signaling that reserves were nearing ample levels and indicating important changes in money market conditions.

Since the start of the balance sheet runoff, the EFFR has mostly traded at 7 basis points below the IORB rate, with occasional dips to 8 basis points below. The inflection point came between September and December 2025, when, amid declining reserves and substantial Treasury issuance, overnight repo rates began to rise and remained consistently above the EFFR. The Federal Home Loan Banks (FHLBs)—the predominant lenders in the federal funds market—responded by reallocating some lending from federal funds to reverse repos, where they could earn better returns, and demanding higher rates on their remaining federal funds lending. Over the course of just three months toward the end of 2025, the EFFR rose from 7 basis points below IORB to just 1 basis point below IORB. This shift illustrated the interconnected nature of money markets. The tightening EFFR-IORB spread served as a signal that reserve conditions were moving from abundant toward ample—though it represented just one indicator among many.

EFFR-IORB Spread and Fed Funds Volumes

A Multidimensional View of Reserve Demand

While Box 1 describes a specific market indicator, the changing reserves environment during 2025 also required monitoring how reserve demand was shifting. The Desk monitors many money market indicators to evaluate reserve demand, and price signals alone don’t tell the whole story, as Box 2 in the SOMA Annual Report explains.

The Federal Reserve gauges shifts in reserve demand by conducting outreach to market participants, including through the Senior Financial Officer Survey (SFOS), which is conducted twice a year. The SFOS asks bank treasurers a number of questions in an effort to understand what drives reserve demand. Banks hold reserves for three main reasons: to meet daily payment and settlement needs, to satisfy regulatory liquidity requirements, and to maintain precautionary buffers for potential market shifts.

Both the SFOS results and discussions with market participants showed that reserve demand among banks can fluctuate as incentives to hold reserves change with market conditions. Surveys during 2025, along with other market indicators, suggested that bank reserve management behavior had shifted and reserves were approaching ample levels.

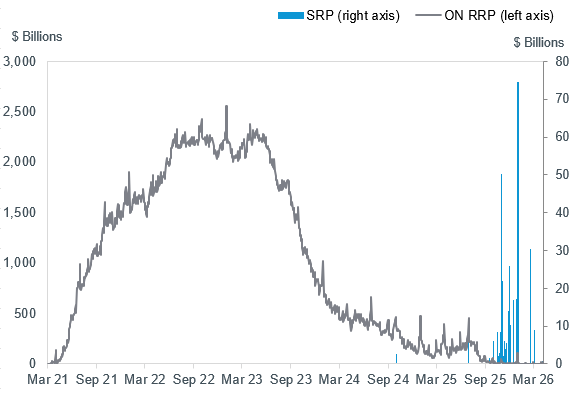

To understand reserve demand, the Fed also uses economic models, bank-level data on actual reserve management, and monitoring of Federal Reserve operations usage. For example, increased usage of standing repo (SRP) operations during the second half of the year was one indicator suggesting that reserve conditions were approaching ample.

ON RRP and SRP Operations Volumes

Implementing Reserve Management Purchases

Once the FOMC concluded its balance sheet reduction in December 2025, it directed the Desk to begin conducting RMPs to maintain ample reserves going forward.

In an ample reserves environment, interest rate control is achieved primarily through administered rates, rather than by conducting frequent market interventions to fine-tune the supply of reserves. RMPs are necessary because several Fed liabilities tend to grow alongside the broader economy over time, as Box 3 in the SOMA Annual Report explains. If reserves were not added over time through RMPs, the growth in other Federal Reserve liabilities would eventually cause reserves to fall below the range the Committee deems to be ample. (As SOMA Manager Roberto Perli said in a recent speech, RMPs do not represent a change in the stance of monetary policy.)

The Desk determines its purchase plans by analyzing money market conditions, its forecast for Federal Reserve liabilities, and its projections for reserve demand. Ahead of periods of substantial expected growth in liabilities, the Desk may increase the pace of purchases. The Desk also seeks to smooth purchases over several months to avoid concentrated buying during periods of seasonal volatility.

The Fed’s SRP and ON RRP complement RMPs to ensure effective rate control. When reserves move to higher levels within the ample range, ON RRP operations could, in principle, absorb excess liquidity. At lower levels, SRP operations provide additional reserves if needed. Together, the actions outlined in the SOMA Annual Report’s three special sections—monitoring market indicators, assessing reserve demand, and calibrating RMP operations—describe an integrated approach to maintaining ample reserves. The Desk’s continuous monitoring of money market conditions and reserve demand directly informs both the pace and timing of its purchase operations, ensuring reserves remain sufficient to support effective monetary policy implementation.

Following the Data

The Fed provides several public resources to track and understand the evolution of RMPs and the Fed’s balance sheet. The Desk publishes its tentative schedule for its reinvestment and RMP purchases around the ninth business day of each month. All results from daily operations conducted by the Desk are posted on the New York Fed’s website. The Senior Financial Officer Survey is conducted twice a year and is available on the Federal Reserve Board’s website. And the weekly H.4.1 statistical release lists the Federal Reserve’s assets and liabilities, allowing observers to monitor changes in the balance sheet and reserve levels over time. These tools, combined with periodic communication from Fed officials, offer insight into how the Fed maintains ample reserves and implements monetary policy effectively. For a full picture of open market operations in 2025, please see the 2025 SOMA Annual Report.

Christian Cabanilla is an advisor in the New York Fed’s Markets Group.

Natalie Leonard is an associate in the New York Fed’s Markets Group.

Leonard Wei is an associate in the New York Fed’s Markets Group.

The views expressed in this article are those of the contributing authors and do not necessarily reflect the position of the New York Fed or the Federal Reserve System.