In December 2025, the Federal Open Market Committee (FOMC) determined that reserves had declined to ample levels and, consistent with its May 2022 plans, instructed the New York Fed’s Open Market Trading Desk (the Desk) to begin reserve management purchases (RMPs) to maintain reserves within an ample range. These RMPs—which increase the size of the Fed’s balance sheet and the amount of reserves in the banking system—would consist of Treasury bills and, if needed, other Treasury securities with remaining maturities of three years or less.

In this article we summarize the conditions leading to the decision to start RMPs, a key factor driving monthly purchase amounts to date, and how purchase amounts may evolve in the future. For more details, see recent speeches by Roberto Perli, manager of the Federal Reserve’s System Open Market Account (SOMA), and by Julie Remache, deputy SOMA manager.

The Transition from Abundant to Ample Reserves

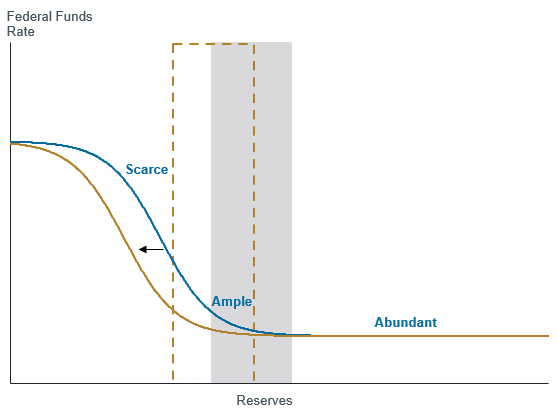

The Federal Reserve implements monetary policy through an ample reserves framework—meaning that it supplies enough reserves to control short-term interest rates primarily through administered rates, rather than through active management of the supply of reserves.

The term “ample” does not refer to a specific quantity of reserves, but rather to a range of reserves that makes the federal funds rate (the Fed’s target rate) only modestly sensitive to short-term variations in reserve supply. When reserve supply is greater than ample (a regime of “abundant” reserves), the fed funds rate is unresponsive to changes in reserve supply, and the quantity of reserves exceeds amounts needed for effective rate control. Conversely, when reserve supply is less than ample (a regime of “scarce” reserves), the fed funds rate responds more forcefully to changes in reserve supply and is significantly more volatile, making rate control more challenging.

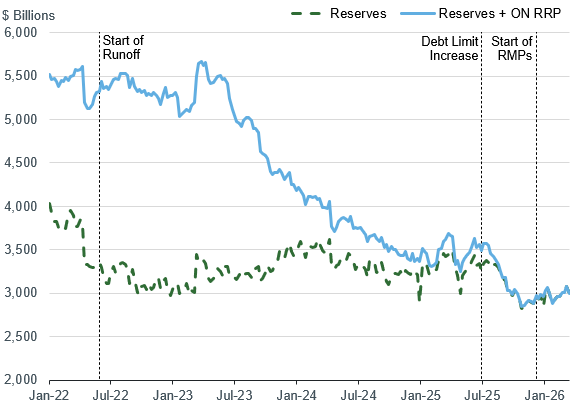

The expansion of the Fed’s balance sheet following the COVID-19 pandemic resulted in abundant reserves. In June 2022, the Fed began significantly reducing its SOMA securities portfolio to bring holdings down to levels needed to implement monetary policy efficiently and effectively in an ample reserves regime.

From the start of balance sheet runoff through last summer, there were incremental signs of money market tightening, but overall reserve conditions remained abundant. Dynamics stemming from the federal debt limit complicated the picture in the first half of 2025, however, by temporarily boosting liquidity in the banking system; this is because the Treasury reduced the amount it deposited at the Fed in the Treasury General Account (TGA)—essentially the U.S. Treasury’s checking account at the Fed—to stay under the debt limit. After the debt limit was increased in July 2025, the U.S. Treasury rapidly replenished the TGA. This, alongside cumulative effects of balance sheet runoff, brought banking system liquidity to the lowest levels since runoff began (see the blue line in the chart below), which induced a notable tightening in money market conditions.

Reserves and ON RRP

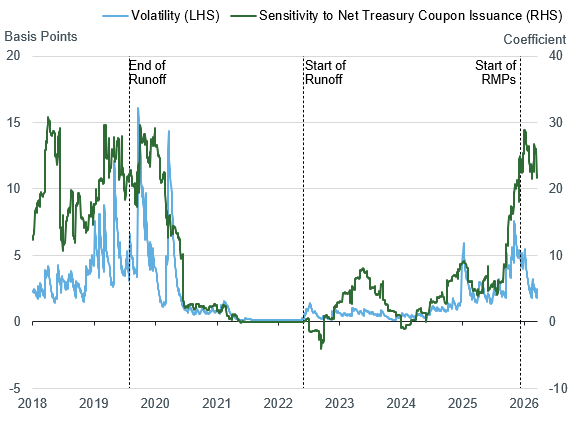

There were numerous signs of tighter conditions: for example, repo reference rates rose relative to the Fed’s administered rates and became more volatile and sensitive to Treasury issuance (see chart below). Amid firmer and more volatile repo market conditions, usage of the Fed’s standing repo operations became larger and more frequent. Higher repo rates contributed to a rapid increase in the fed funds rate.

Volatility and Sensitivity to Net Treasury Coupon Issuance of TGCR

Source: Board of Governors of the Federal Reserve System, Federal Reserve Bank of New York, U.S. Treasury

By December, there was clear evidence from these and other indicators that reserves had transitioned from abundant to ample. Consistent with that, the FOMC instructed the Desk to begin RMPs to maintain reserves within the ample range.

RMP Amounts to Date

The Desk has conducted RMPs at a monthly pace of $40 billion since mid-December (more on the mid-month timing below). It is important to note that money market conditions in late 2025 did not require an immediate injection of reserves at this elevated pace to maintain rate control. However, the Desk anticipated a large and rapid drain of reserves in April amid tax-season-related payment flows into the TGA. Absent any action, there was a high likelihood that those flows would have pushed reserves below the ample range in April, potentially creating challenges for effective rate control. Rather than wait until April and purchase large amounts of securities in a short period of time to offset the expected decline in reserves (an approach that would have been impractical from an implementation perspective), the FOMC opted for a prudent and gradual approach and decided instead to smooth out the required purchases over a longer period of time, starting in December.

The Outlook for RMPs and the Balance Sheet

After the TGA peaks in April, there won’t be a need to continue RMPs at the present elevated pace, consistent with the Desk’s December statement. Accordingly, the monthly RMP pace is likely to be significantly reduced beginning with the purchase period spanning mid-April to mid-May; to account for uncertainty and other factors, the reduction may be somewhat gradual.

Looking further ahead, the size of RMPs required to maintain ample reserves need not be constant—RMPs will be largely driven by trend growth and variation in Federal Reserve liabilities, with the Desk’s assessment of money market conditions serving both as a critical input and important feedback mechanism. Flexibility in the monthly pace of RMPs over time allows the Desk to address changes in factors that at times materially drain and add reserves.

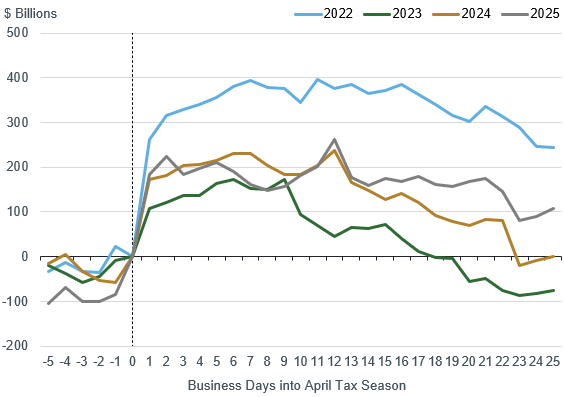

Currency (Federal Reserve notes), the TGA, and reserves are particularly important as they comprise over 90 percent of current Fed liabilities. Currency has historically grown with nominal economic growth and international demand for the U.S. dollar. The TGA has also grown in nominal terms over time and has significant seasonal variation. For example, over the past several years, the TGA has risen somewhere between roughly $175 billion and $400 billion during April tax season (see chart below) and generally has gradually declined to more normal levels thereafter.

Cumulative Changes in TGA (Indexed to Day Before Mid-April Tax Day)

All else equal, reserve demand may be expected to grow over time with bank assets and bank payment volumes. But, importantly, structural changes in the banking system can lead to changes in reserve demand. In particular, future potential changes to bank regulatory liquidity requirements may eventually reduce demand for reserves. If that were to happen, the quantity of reserves consistent with an ample reserves regime would be smaller than it otherwise would be (as illustrated in chart below), and the Desk would take that into account when formulating a plan for the size of the SOMA portfolio.

Stylized Reserve Demand Curve

Details on RMP Operations

To date, RMPs have been conducted entirely in Treasury bills. These bill purchases have been running smoothly, with little market impact— and this is expected to continue. However, should continued bill purchases lead to strains in the bill market, the Desk has the flexibility to purchase short-term Treasury coupon securities to preserve bill market functioning. The Desk could also revert to Treasury coupon purchases if the FOMC decided that the share of bills in the SOMA portfolio has reached its desired level.

The Desk announces monthly purchase amounts on or around the ninth business day of each month alongside a tentative schedule of purchase operations for the next monthly period. Purchase periods are defined on a mid-month to mid-month basis to incorporate information released early each calendar month on funds to be received from agency MBS principal payments.

The New York Fed’s website posts details on individual purchase operations and SOMA securities holdings. Additional information on the Federal Reserve’s balance sheet is available weekly through the Federal Reserve Board’s H.4.1 release.

Roberto Perli is the Manager of the System Open Market Account (SOMA) and a senior leader in the New York Fed’s Markets Group.

Eric LeSueur is an advisor in the New York Fed’s Markets Group.

Linsey Molloy is an associate director in the New York Fed’s Markets Group.

The views expressed in this article are those of the contributing authors and do not necessarily reflect the position of the New York Fed or the Federal Reserve System.