The rise in inflation following the COVID-19 pandemic was a global phenomenon, and it prompted many central banks to tighten monetary policy to bring inflation down. A recently published Centre for Economic Policy Research e-book, “Monetary Policy Responses to the Post-Pandemic Inflation,” provides a collection of viewpoints on the actions of central banks and their effects across various economies and markets.

We were pleased to contribute a chapter discussing the effects of inflation and the Federal Reserve’s policy tightening response on U.S. financial markets. In this article, we highlight key themes from our chapter. While it is too soon to draw definitive conclusions about this inflation episode—especially since the disinflation process is ongoing and policy is evolving—we can make some observations based on the experience to date.

The Post-COVID Inflation Surprise

The extent and duration of the recent high inflation in the U.S. notably exceeded market-implied expectations and most forecasts (such as those from our Desk surveys and even those of policymakers). As one example, market expectations for Consumer Price Index (CPI) inflation—as shown by the light green lines in Figure 1—considerably undershot the actual CPI path during 2021 through mid-2022.

Figure 1

The reasons for such considerable misses are a topic for broader research. But, at a high level, we would note that the U.S. economy had to contend with supply chain difficulties induced by a once-in-a-century pandemic, the subsequent aggregate demand surge spurred by pent-up demand and the fiscal and monetary policy responses to the pandemic, and the spike in global energy prices that followed the beginning of Russia’s war against Ukraine. These events were difficult to anticipate and well outside recent experience, which made estimating their effects challenging even after they occurred.

The Federal Reserve’s Response

In light of these inflation dynamics, the Federal Reserve responded more forcefully than both markets and policymakers themselves had anticipated.

The policy adjustment process began from a very accommodative starting point. The Federal Reserve’s targeted interest rate—the federal funds rate—had been brought down to around zero in March 2020. Additionally, the Federal Reserve’s balance sheet had expanded significantly due to asset purchases that were implemented initially to restore market functioning and subsequently to support the economic recovery.

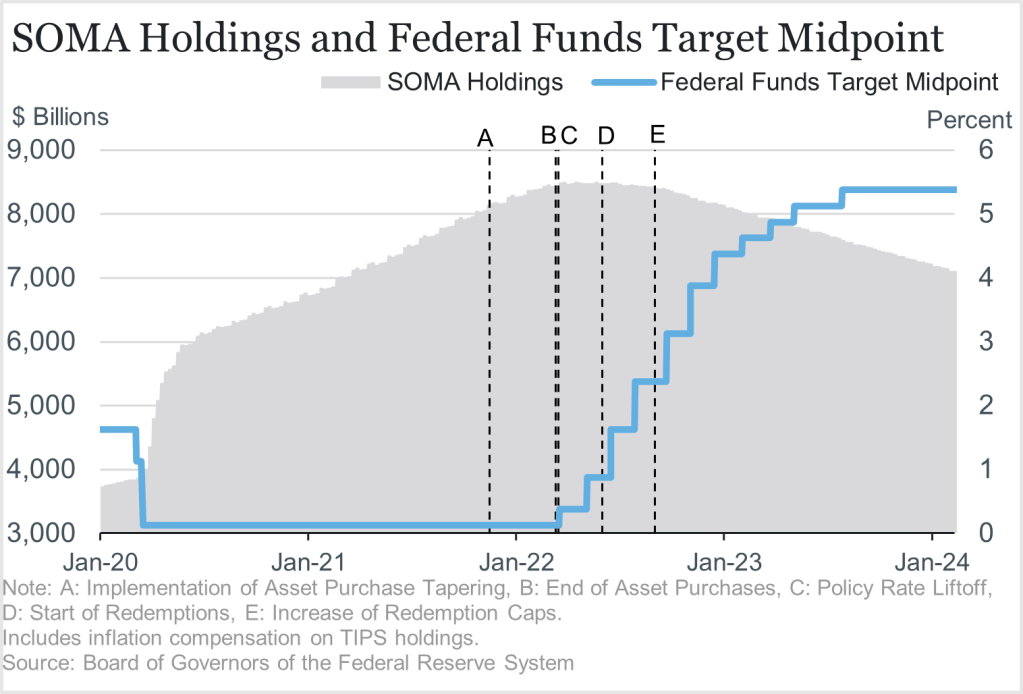

The process of moving to a less accommodative stance began with communication and slowing asset purchases. Rate hikes began in March 2022, soon after the conclusion of the asset purchase program (Figure 2). The pace was initially moderate, but given continued high inflation, it accelerated to include four consecutive 75-basis-point moves between June and November 2022. The pace then moderated as inflation began to recede and policymakers judged that the stance of policy was approaching a level that would be sufficiently restrictive to return inflation to their target over time.

Figure 2

Consistent with past tightening cycles, changes to the federal funds rate were the primary instrument for tightening monetary policy. Still, policy was also tightened by reductions in the size of the Federal Reserve’s balance sheet, beginning in June 2022.

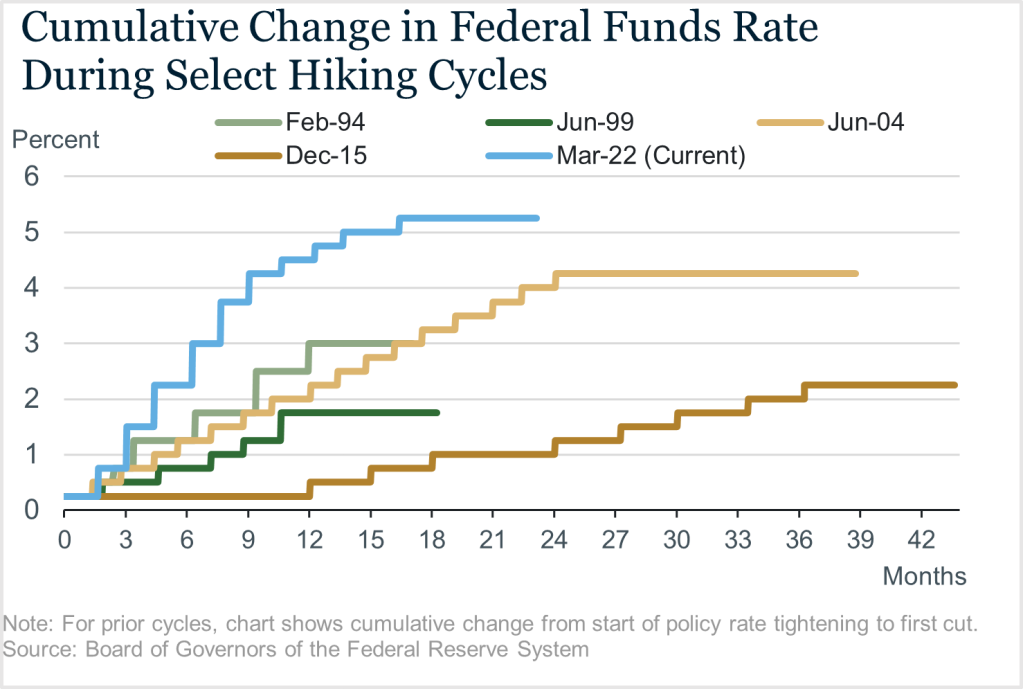

Cumulatively, the policy response resulted in the most aggressive rate hiking cycle in decades (Figure 3) and in a faster pace of balance sheet reduction than over the period from 2017 to 2019. In any circumstance, a tightening cycle of such magnitude could be expected to prompt significant changes in asset prices—and large moves surely occurred.

Figure 3

Financial Conditions

In response to the Fed’s policy actions, financial conditions tightened at a pace rarely experienced over the past four decades. Some of the key market developments included a rise in Treasury yields (especially shorter-term yields more sensitive to monetary policy expectations), a related increase in borrowing costs for households and corporations, downward pressure on equity prices, and a strengthening of the U.S. dollar against other currencies. In aggregate, the change in financial conditions was sharp on a standalone basis and relative to prior hiking cycles over recent decades.

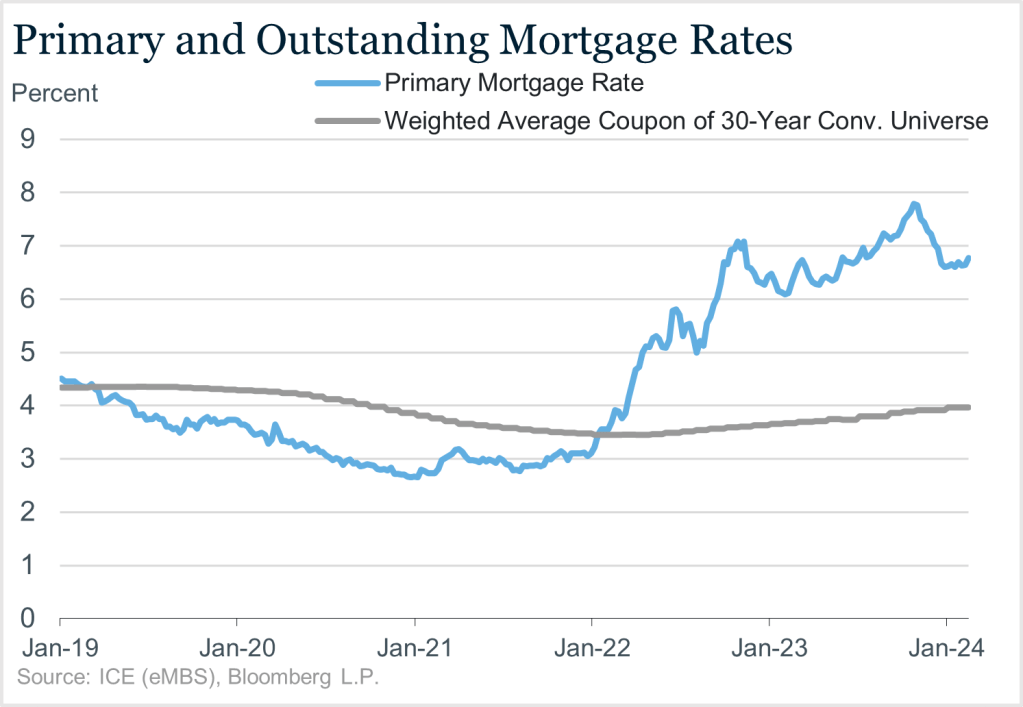

Still, the transmission of tighter policy varied across markets and economic sectors. For example, mortgage rates rose as high as 8 percent, from less than 3 percent in early 2021 (see blue line in Figure 4). The sharp rise in borrowing costs dampened new borrowing activity and refinancing incentives, and strongly disincentivized moving and homebuying for households. As a result, existing home sales fell sharply. But this also meant that the average rate across all existing mortgages only rose very gradually (see gray line in Figure 4). A way to interpret this is that monetary policy decisions passed through slowly to the household sector in certain respects.

Figure 4

Despite large changes in asset prices, financial stress was relatively contained compared to some past episodes, although the banking sector concerns in early 2023 were notable. Treasury market liquidity was challenged over the tightening cycle, but overall was consistent with the elevated levels of volatility (as discussed at the 2023 U.S. Treasury Market Conference).

Monetary Policy Implementation

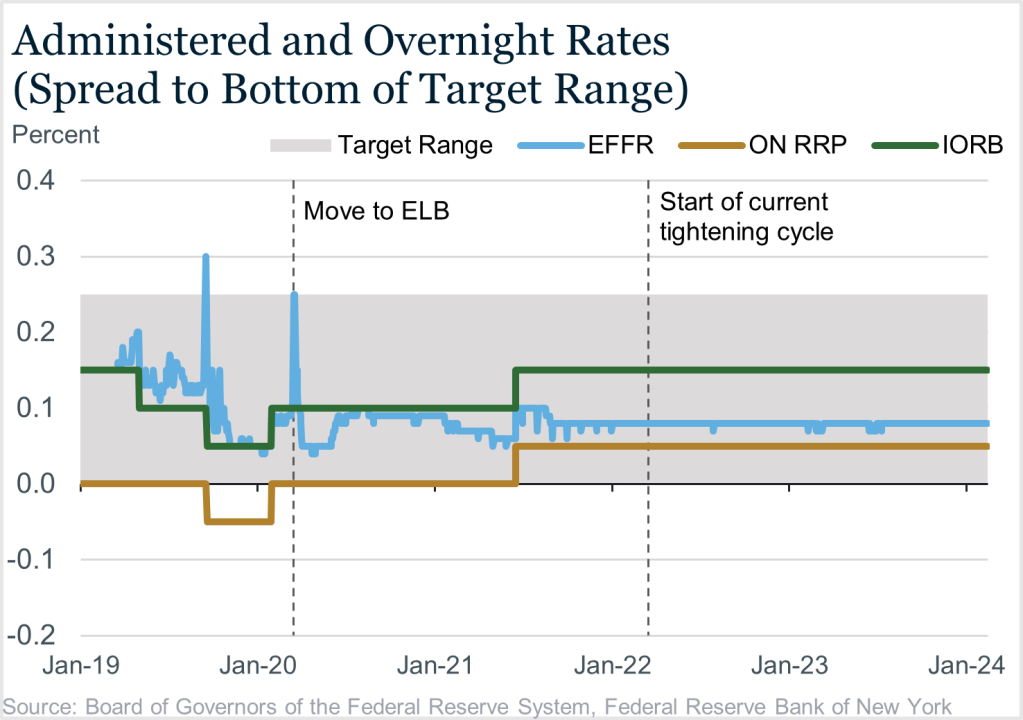

Effective monetary policy implementation is critical for the Federal Reserve to be able to meet its mandated objectives of maximum employment and price stability. The Fed’s framework for implementing monetary policy achieves interest rate control primarily through administered rates rather than active management of the supply of reserves.

This framework has worked well throughout this inflationary period. Even amid significant changes in the monetary policy stance and episodes of stress in money markets (as discussed in this speech), overnight rate control remained very strong, with the federal funds rate moving as Fed policymakers intended. Indeed, not only has the federal funds rate remained well within the target range since the start of the pandemic and subsequent events, but its volatility relative to administered rates has been historically low (Figure 5). Overall, the mechanics of monetary policy implementation have so far not been affected by the high inflation and subsequent policy response.

Figure 5

The balance sheet reduction process has also gone smoothly, with no signs of adverse effects on market functioning. The performance of the Fed’s operating framework and balance sheet reduction process should support market confidence that the Federal Reserve has the appropriate tools to implement a tightening of monetary policy.

Longer-term Inflation Expectations

An important concluding observation is that longer-term inflation expectations have remained well anchored around the Fed’s long run objective of 2 percent. Near-term inflation expectations were volatile, largely tracking changes in the actual path of inflation. But inflation expectations for just a few years out stayed at levels consistent with the Federal Reserve’s target throughout this inflationary episode. We attribute this to the credibility the Federal Reserve has accumulated over the years about its determination to keep inflation at its long-run objective. In the absence of such credibility, inflation may have increased more significantly, and substantially tighter policy—with all its consequences on the employment side of the Federal Reserve’s mandate—may have been necessary to regain control of inflation.

See the full e-book published by the Centre for Economic Policy Research (CEPR), including Chapter 20 by the authors.

Roberto Perli is the Manager of the System Open Market Account (SOMA) and a senior leader in the New York Fed’s Markets Group.

Eric LeSueur is a policy and market analysis advisor in the New York Fed’s Markets Group.

The views expressed in this article are those of the contributing authors and do not necessarily reflect the position of the New York Fed or the Federal Reserve System.