The Federal Open Market Committee (FOMC) is responsible for conducting U.S. monetary policy to promote maximum employment and stable prices. The FOMC’s primary tool for adjusting the stance of monetary policy is by setting and adjusting the target range for the federal funds rate, which is the rate at which banks and other eligible Federal Reserve account holders borrow and lend reserves between each other on an overnight basis. In the Fed’s ample reserves implementation framework, the federal funds rate is kept within the target range primarily through the setting of administered rates, which are rates set directly by the Fed rather than by market forces, in conjunction with the Fed supplying sufficient levels of reserves to the banking system.

Standing Repo Operations in an Ample Reserves Framework

At times, the demand for reserves can exceed supply, which may lead to increases in the federal funds rate. To help ensure the federal funds rate does not exceed the target range, the New York Fed’s Open Market Trading Desk (the Desk) executes repurchase agreement (repo) transactions twice a day with eligible counterparties, which include all primary dealers and certain banks, via Standing Repo operations (SRPs). SRPs provide a reliable, alternative source of overnight funding at an administered interest rate (the “SRP rate”), currently set at the top of the federal funds target range. In an SRP transaction, the Desk purchases securities from a counterparty and simultaneously agrees to resell those securities the following business day. SRPs help limit upward pressure in private market repo rates because counterparties should be willing to source funding from the Fed via SRPs when economically sensible; that is, when private market repo rates for government securities exceed the SRP rate.

This article highlights results from a recent Desk survey of primary dealers and the Fed’s Senior Financial Officer Survey, which surveys banks, on factors influencing their willingness to use SRPs. The surveys encompass all SRP counterparties and suggest their willingness to use SRPs has improved recently in response to operational changes and Fed communications. Improved willingness to use SRPs enhances the effectiveness of these open market operations and, as a result, the implementation of monetary policy.

Why Counterparties Use Standing Repo Operations

Counterparties use SRPs in the context of their business models to support repo market intermediation or to raise reserves, when economically sensible. As intermediaries, primary dealers facilitate the flow of cash between clients and rely on repo markets as a primary source of funding. These counterparties would mainly use SRPs as an alternative funding source when private market repo rates exceed the SRP rate, allowing them to obtain funding at a relatively lower rate and then distribute it to other market participants. Counterparties that are not repo market intermediaries, such as certain banks, would mainly use SRPs to convert high-quality, liquid security holdings into reserves. For example, a bank facing a payment need could use SRPs to obtain cash secured by eligible securities held in their liquidity portfolios to meet this payment need when private market repo rates exceed the SRP rate.

Key SRP-Related Takeaways from the Surveys

Experiences in past years indicated counterparties encountered a variety of frictions to using SRPs when economically sensible. However, results from the most recent surveys suggest counterparties are more willing than in past years to use SRPs following recent operational changes and related Fed communications. Survey results also suggest counterparties are willing to use SRPs when private market repo rates only modestly exceed the SRP rate, though certain frictions remain.

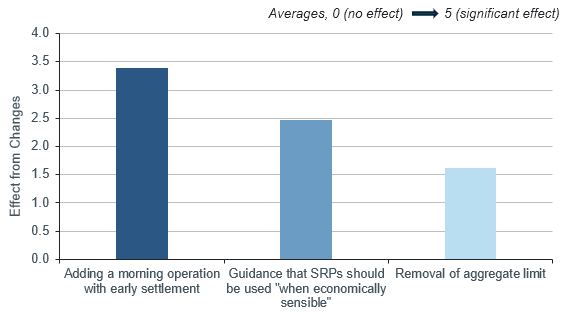

Primary dealers indicated that the addition of a morning, early-settling SRP operation in June 2025 and communications from Fed officials stating that SRPs should be used when economically sensible had the most positive impacts, as seen in Figures 1 and 3. These communications include speeches from New York Fed President John Williams and SOMA Manager Roberto Perli, and remarks by Chair Jerome Powell during his December 2025 FOMC press conference. Other factors noted as improving counterparties’ willingness to use SRPs include removing the aggregate operation limit to provide counterparties certainty over the availability of SRP-based funding, and observing increases in usage over time.

Figure 1: Primary Dealers’ Views on Recent Changes to SRPs

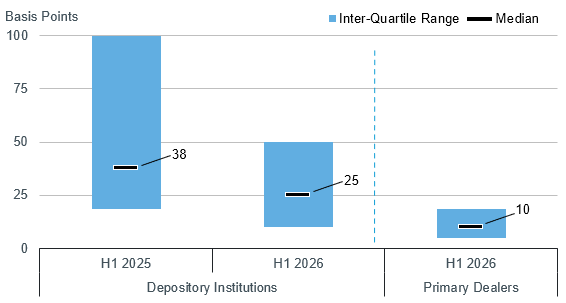

Survey results also show counterparties are willing to use SRPs when private market repo rates only modestly exceed the SRP rate, which should further support effective monetary policy implementation. As seen in Figure 2, primary dealers’ median response indicated they are willing to use SRPs when private market repo rates rise 10 basis points above the SRP rate, which we refer to as the “hurdle spread.” For banks, the median hurdle spread narrowed to 25 basis points, from 38 basis points in the last survey. Counterparties’ hurdle spreads reflect non-price factors they face when deciding to use SRPs, such as the lack of balance sheet netting offered to counterparties when transacting in SRPs, which we discuss in more detail below.

Figure 2: Median Hurdle Spreads to “Actively Consider” Using SRPs

Source: Senior Financial Officer Survey and Primary Dealer SRP Survey.

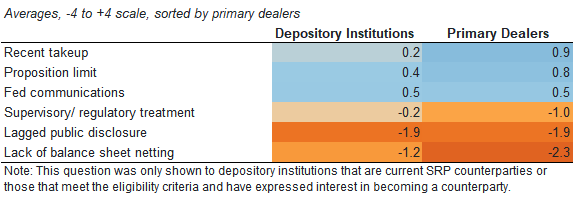

Counterparties highlighted a few factors that make them reluctant to use SRPs, shown in Figure 3. The most significant contributor to primary dealers’ reluctance was the inability to “net” SRP transactions against other client activity to reduce balance sheet costs. Repo market intermediaries commonly net repo and reverse repo transactions for accounting purposes, often by centrally clearing transactions through central counterparties (CCPs), but the Fed does not currently offer a mechanism to centrally clear SRP transactions. CCPs become the buyer to every seller and seller to every buyer, making them the legal counterparty to intermediaries’ repo and reverse repo transactions, which allows counterparties to net down these transactions for accounting purposes. Many primary dealers indicated in survey responses that their willingness to use SRPs would increase meaningfully if SRP transactions were centrally cleared. Respondents also noted that the legally required two-year lagged public disclosure of SRP transactions was a strongly discouraging factor.

Figure 3: Factors Affecting SRP Participation

Conclusion

Results from these recent surveys provide the Desk with a better understanding of potential SRP usage and how SRPs support monetary policy implementation and smooth market functioning. Survey results indicate recent changes and related Fed communications around SRPs have improved counterparties’ willingness to use these open market operations, which will continue to support effective policy implementation. At the same time, counterparties continue to point to factors that discourage use of SRPs when economically sensible, such as supervisory treatment, lagged public disclosures, and lack of netting opportunities, which some noted could be addressed by centrally clearing the operations. These may be areas of further study.

We would like to acknowledge our Markets Group colleagues Sean Fulmer and Natalie Leonard for their contributions to this article.

Dean Friedberg is an associate in the New York Fed’s Markets Group.

Michael Koslow is an associate director in the New York Fed’s Markets Group.

Jason Miu is an associate director in the New York Fed’s Markets Group.

Roberto Perli is the Manager of the System Open Market Account (SOMA) and a senior leader in the New York Fed’s Markets Group.

The views expressed in this article are those of the contributing authors and do not necessarily reflect the position of the New York Fed or the Federal Reserve System.