In recent articles, we introduced the Fed’s policy implementation framework, the role of the Fed’s balance sheet, and the Fed’s standing liquidity facilities. In this article, we use those key concepts to discuss recent developments in monetary policy implementation and how the Fed’s tools work in practice.

The rise in inflation in the years following the COVID-19 pandemic prompted the Federal Open Market Committee (FOMC) to significantly tighten the stance of monetary policy to return inflation back to its target of 2 percent over time.

The FOMC uses the federal funds target range as the primary tool for tightening the stance of monetary policy, and in March 2022, began raising the target range. The FOMC also tightened monetary policy by reducing the securities holdings on its balance sheet, starting in mid-2022.

Interest Rate Control

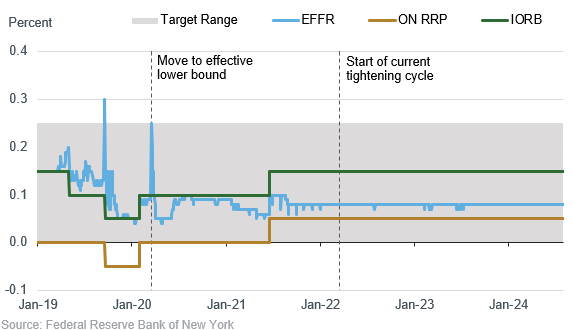

As noted in previous articles, control of short-term interest rates is essential to effectively implement monetary policy. Keeping the effective federal funds rate (EFFR) well within the FOMC’s target range allows market participants to maintain confidence in the level of short-term interest rates and sets the basis for expectations on longer-term interest rates and broader financial conditions.

The Fed has maintained the EFFR within its target range in recent years despite significant increases in the target range and unexpected market events, like the banking sector stress in early 2023.

One simple way to illustrate this is to look at where the EFFR has been relative to the Fed’s target range and its administered rates, which are the interest rate on reserve balances (IORB) and the interest rate on the overnight reverse repo (ON RRP) facility. As seen below, the EFFR has remained stable within the target range (the shaded area) ever since the Fed started tightening policy in 2022. This high degree of interest rate control shows the strong performance of the Fed’s policy implementation tools.

Administered and Overnight Rates

(Spread to Bottom of Target Range)

Specifically, the IORB and the ON RRP have, as designed, been effective in providing a floor under short-term interest rates. As the Fed increased its administered rates, it maintained strong control over short-term rates, with the EFFR and other overnight interest rates moving in line with increases in the target range. The Fed’s standing liquidity facilities, such as the discount window, have also worked to counteract any potential unexpected upward pressures in money market rates, though they have been little used given abundant liquidity in the banking system.

Strong control of short-term interest rates has enabled monetary policy decisions to transmit to broader markets and the economy. In particular, expectations that the federal funds rate would remain high have translated into higher long-term interest rates, like interest rates on new business loans, consumer loans, and mortgages. Raising such borrowing costs has helped moderate demand and bring down inflation.

Balance Sheet Reduction

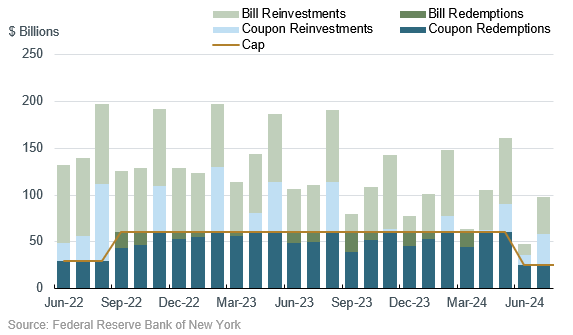

Along with the increases in the federal funds target range, the FOMC has also significantly reduced the size of its balance sheet. The FOMC outlined balance sheet reduction principles in January 2022 and more specific plans in May 2022 to guide the ongoing reduction and ensure a smooth transition from an abundant to ample supply of reserves. The plans communicated by the FOMC in May 2022 indicated that securities held by the Fed would be allowed to decrease up to certain monthly limits, or caps, to provide predictability on the amount of runoff that could occur each month.

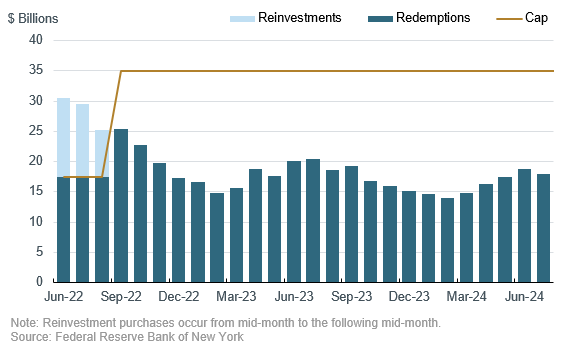

Since the start of balance sheet runoff in June 2022 through July 2024, the Fed’s securities holdings decreased by a total of $1.75 trillion, reflecting a $1.36 trillion reduction in Treasury securities and $0.39 trillion reduction in agency mortgage-backed securities (MBS) holdings (see below). In May 2024, the FOMC announced that it would slow the pace of balance sheet reduction, lowering the cap on Treasury redemptions effective June 2024.

Treasury Redemptions and Reinvestments

Agency MBS Redemptions and Reinvestments

While the balance sheet’s overall size has decreased alongside the reduction in securities holdings, the composition of Fed liabilities has also been changing. In particular, the decrease in Fed liabilities since securities runoff began in June 2022 has come almost entirely from the ON RRP facility, leaving other Fed liabilities little changed on net.

Usage of the ON RRP facility has, as intended, been responsive to interest rates on alternative investments. Following the post-pandemic expansion of the Fed’s balance sheet, ON RRP facility usage was large because it was an economically attractive money market investment option and served as an outlet for the abundant liquidity in the banking system. More recently, as alternative money market investments such as Treasury bills and private repo started offering slightly higher rates than the ON RRP facility, ON RRP counterparties responded by reallocating away from the facility and toward other investments. At some point, when the ON RRP reaches zero or otherwise stabilizes, reserves will start declining roughly one-for-one with balance sheet runoff, all else equal.

Going forward, the FOMC intends to stop reducing the balance sheet once reserves are somewhat above the level it judges to be consistent with an ample supply of reserves, as stated in its May 2022 plans. At that point, the Fed’s securities holdings will be held constant, but reserve balances will continue to decline over time, all else equal, reflecting growth in other Federal Reserve liabilities, like currency. When the FOMC judges that reserve balances are at an ample level, it will start managing the Fed’s securities holdings as needed to maintain an ample level of reserves over time.

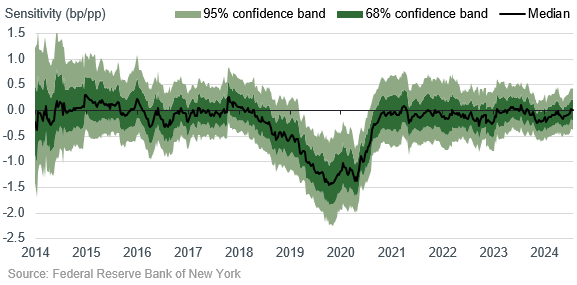

The specific level of reserves that is consistent with ample reserves is hard to anticipate with certainty. In a May 2024 speech, SOMA Manager Roberto Perli discussed some of the indicators Fed staff are monitoring to understand when reserves may be approaching that threshold. Overall, those indicators continue to suggest reserves remain abundant. For example, the EFFR has been completely stable relative to IORB. The federal funds market also remains unresponsive to temporary changes in reserve supply (see below). Additionally, although peak daylight overdraft activity has picked up somewhat, average daylight overdraft activity (a better measure of overall liquidity conditions) has been more stable.

Sensitivity of the Fed Funds Rate to the Quantity of Reserves

That said, we do see some signs of upward pressure on secured money market rates. Higher repo rates appear to be related to distributional frictions and other idiosyncratic factors rather than overall reserve supply and could prove temporary. But they are, as always, important to monitor and assess.

Recent developments also highlight the underlying logic of the FOMC’s recently announced reduction in the pace of runoff. The FOMC recognizes that forecasting reserve demand is highly uncertain. A slower pace of runoff provides more time to monitor money market conditions, for market participants to adapt, and to determine when the reserve supply is starting to shift from abundant to ample.

Looking ahead, the FOMC has three policy meetings planned for the rest of 2024: in September, November, and December. If you’re interested in following developments from those meetings, bookmark this page for the latest FOMC statements and to watch the press conferences. To get the latest updates right in your inbox, subscribe to the New York Fed’s Markets & Policy Implementation list or to alerts from the Board of Governors.

Thank you for working your way through our monetary policy implementation “summer reading list.” We encourage you to explore our website for a much deeper dive into our work!

Christian Cabanilla is an advisor in the New York Fed’s Markets Group.

Eric LeSueur is an advisor in the New York Fed’s Markets Group.

Josh Younger is an advisor in the New York Fed’s Markets Group.

Also in this series:

The views expressed in this article are those of the contributing authors and do not necessarily reflect the position of the New York Fed or the Federal Reserve System.